English

English français

français Deutsch

Deutsch русский

русский español

español português

português العربية

العربية 日本語

日本語 한국의

한국의 Tiếng việt

Tiếng việt

Call Us Now

TEL: +86-4000988557;

Teams: gfreex@hotmail.com;

WeChat: Troysupply_com;

QQ ID: 8936906.

Since 2013, China has become the world's largest robot market, ranking first in the world for six consecutive years. my country has become an important production base and consumer market for global robots.

Industrial robots in global operations hit a new highter score

According to the statistics of the International Robot Federation IFR in 2019, there are 2.7 million industrial robots in operation in factories worldwide, an annual increase of 12%, the highest historical record.

From a regional perspective, the largest market in 2019 is Asia. Among them, the number of industrial robots in operation in China increased by 21% annually, to about 783,000 units; the number of industrial robots in operation in Japan was 355,000.

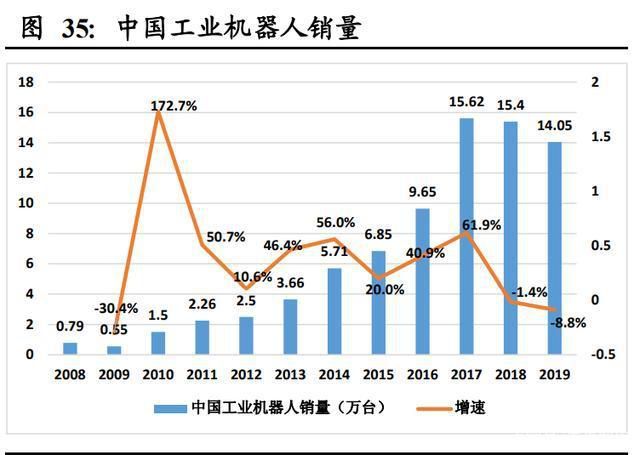

In 2019, the shipment of industrial robots was 373,000 units. In terms of country shipments, China's shipments were 145,000 units, Japan's 49,000 units were second, and the United States was 33,300 units. For the third place.

Among the domestic industrial robot shipments, the four major robot factories including Yaskawa Electric, Fanuc, Abb, and Kuka together account for more than 70%.

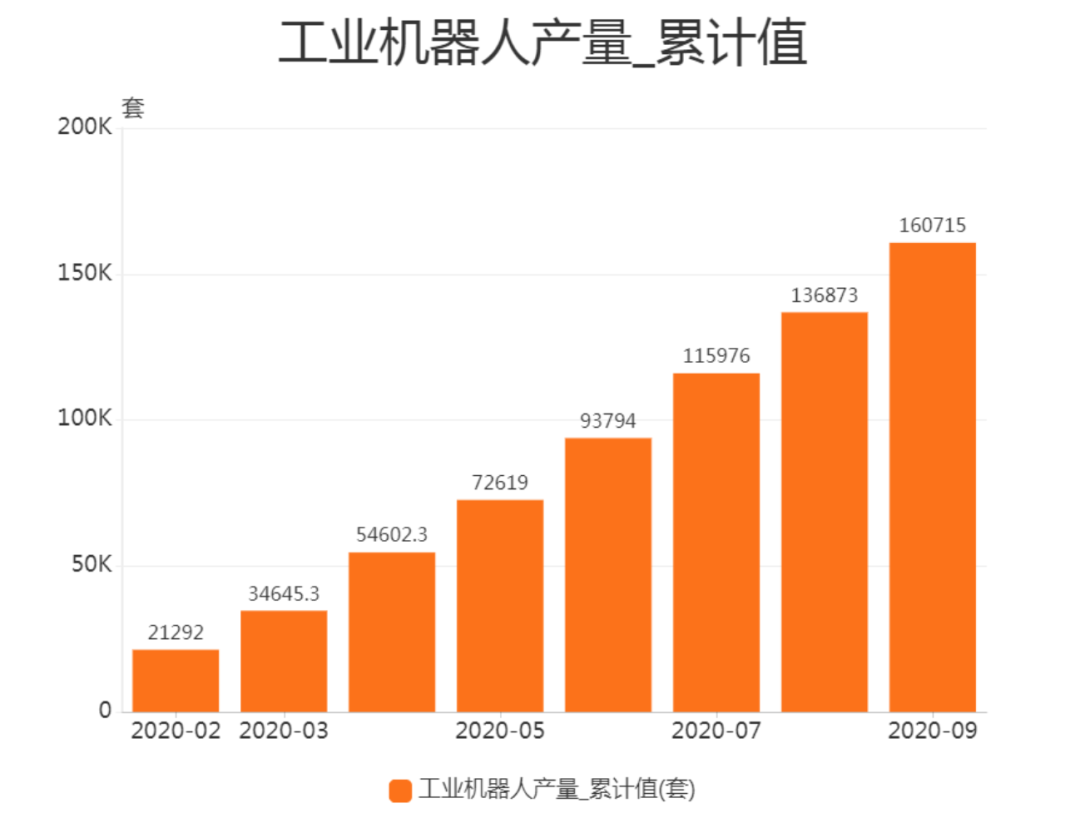

According to statistics from the National Bureau of Statistics, the output of industrial robots in August 2020 was 20,700 units, an increase of 32.50% year-on-year; the output of industrial robots from January to August 2020 was 136,900 units, an increase of 13.90% year-on-year.

The International Federation of Robotics predicts that the growth of global industrial robots will be flat by 2019 and will return to double-digit growth after 2020.

The China Robot Industry Alliance predicts that from 2020 to 2029, the average annual growth rate will be higher than 29%.

Domestic industrial robot sales are increasing year by year

Since 2002, the sales of industrial robots in China have increased rapidly.

In 2003, the sales growth rate of industrial robots in China reached 178%, which was much higher than the world average of 18.8%. Since then, the annual sales volume of industrial robots in China has reached more than 1,000 units.

From 2005 to 2008, the growth rate of my country's industrial robot sales remained in the 20%-30% range.

Affected by the economic crisis in 2009, the growth rate of China's industrial robot sales fell by 30%, but it was still higher than the global level.

From 2010 to 2017, global industrial robot sales have entered a new round of rapid growth (average annual growth rate> 25%), and China's industrial robots have also begun to grow rapidly since 2010.

From 2010 to 2017, it achieved rapid sales growth for 7 consecutive years, with a compound growth rate of 39.8%, which continued to be higher than the global industrial robot sales growth rate.

In 2018 and 2019, affected by the macroeconomic downturn and Sino-US trade friction, the growth rate of China's industrial robot sales has stagnated.

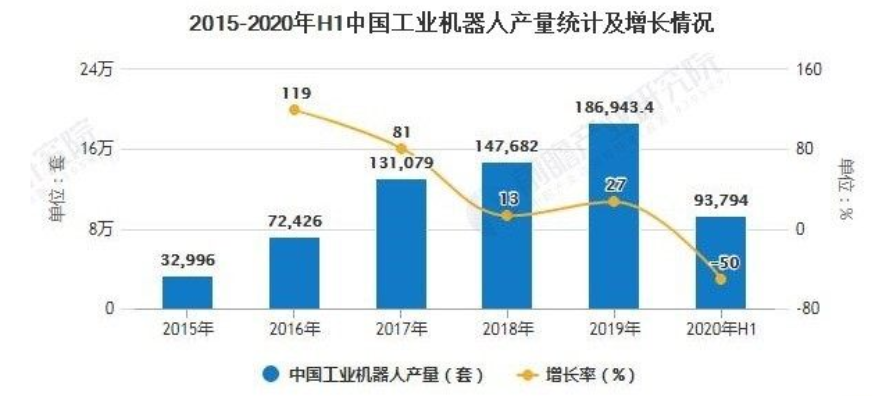

In the first half of 2020, the output of industrial robots will experience negative growth. Affected by the epidemic, the development of downstream robot industries such as domestic automobiles and electronics has been limited, and the growth rate of robot demand has slowed.

Industrial chain of core components + robot body + integrated application

①Upstream core components include control systems, servo motors, precision reducers, and sensors, which are equivalent to the "brain" of the robot.

In terms of competition, foreign-funded enterprises have an absolute advantage. Japanese brands have monopolized the small and medium OEM market (share 45%) with good product performance and extremely competitive prices. European brands have 30% and domestically produced 15%.

②The midstream is the manufacturing of the industrial robot body, which is the "body" of the robot, including arms, wrists, etc. Some robot bodies also include walking structures.

The hardware technology of the robot body has become mature, mainly in the optimization of the structure and the improvement of the user experience. Foreign capital still monopolizes the high-end market, and the localization rate of the low-end and middle-end markets has increased.

Fanuc, ABB, Yaskawa, KUKA's four global robot families account for more than 50% of the total market share.

③The downstream is an integrated application company, responsible for the targeted system integration and software secondary development of industrial robots according to different application scenarios and uses.

Breakthrough progress has been made in the research and development of key common technologies such as dual-arm robot binocular vision positioning technology, flexible gripper design technology, and dual-arm coordinated control technology.

The collaborative robot realizes the integrated integration of reducer, motor, encoder and drive control, and the repeatability of some products can reach plus or minus 0.05 mm.

The economics of "machine substitution" gradually become prominent

In recent years, with the rapid economic growth and the decline in the number of domestic working-age populations, the inflection point of labor supply has appeared, and the demographic dividend has gradually disappeared.

The proportion of the working-age population aged 15-64 in China has declined since 2011;

The absolute number of people aged 15-64 has also entered a decline since 2014;

The population aged 15-64 in 2018 decreased by approximately 12 million from the peak in 2013.

This demographic shift is reflected in the labor market as labor shortages, difficulties in recruiting companies, and expensive recruitment.

The rising labor cost has given birth to the demand for machine substitution.

In addition, since 2012, the global average price of industrial robots has generally shown a steady and declining trend, with rising labor costs and falling robot costs.

In this context, the replacement of labor by machines from 2020 to 2050 may become a long-term development trend with high certainty. The domestic demand for automation and intelligent equipment is expected to continue to increase.

The integration of traditional robots and collaborative robots

At present, human-machine collaboration applications are showing an upward trend. In 2019, the installation data of collaborative robots increased by 11% compared with 2018.

With more and more suppliers launching collaborative robots, the scope of application of this kind of robots is becoming wider and wider.

The field of industrial robots is also combining traditional cage robots that can accurately process tasks with new collaborative robots that can work safely with humans to realize the two collaborative work.

my country's implementation of the "Made in China 2025" strategy is also a policy support for industrial robots in order to promote intelligent manufacturing. Domestic industrial robots are also constantly innovating, and the market has responded well.

ABB, KUKA, Siasun and other industrial robot manufacturers have occupied a place in the field.

In addition to these brands, more small and medium-sized industrial robot manufacturers have become the main force in the industrial robot market.

The rise of domestic industrial robots and industry problems

From 2015 to 2019, in the domestic six-axis robot market, the sales of domestic robots increased from less than 8,000 units to nearly 24,000 units; the domestic market share also increased from 16.4% in 2015 to 2019. 24.1%.

In the gradual development of smart cities and smart factories in the future, industrial robots will play an important role, and a large number of industrial robots are needed for intelligent operation.

The accelerated construction of 5G, Internet of Things, and Industrial Internet is of great significance to the development of industrial robots. It is estimated that by 2025, the industrial robot market will reach nearly 10 billion U.S. dollars.

But according to the GGII agency data, the difficulties of China's industrial robot business in 2019 are mainly due to the lack of integrator capabilities, the long return on investment period, the lack of integrator capabilities, and the need to improve end user awareness.

Although my country is the world's largest consumer market for industrial robots, the market supply is almost mainly completed by foreign-funded enterprises.

In the context of the weakening of the demographic dividend, industrial upgrading and efficiency improvement, "strengthening the industrial foundation and technological innovation capabilities, promoting the integrated development of advanced manufacturing and modern service industries, and accelerating the construction of a manufacturing power" has been clearly written into the government work report, and industrial upgrading Imminent, the general trend of intelligent manufacturing, the explosive period of industrial robots has come.

TEL: +86-4000988557;

Teams: gfreex@hotmail.com;

WeChat: Troysupply_com;

QQ ID: 8936906.

Please read on, stay posted, subscribe, and we welcome you to tell us what you think.

IPv6 network supported 粤ICP备2021036697号

IPv6 network supported 粤ICP备2021036697号 Online service

Online service 4000988557

4000988557 sales1@troysupply.comsales2@troysupply.com

sales1@troysupply.comsales2@troysupply.com Richard Liu

Richard Liu TROY

TROY 8936906

8936906 Troysupply_com

Troysupply_com